International Marine Cargo Insurance: Building generic and thematic competences in commercial translation

Karina Socorro Trujillo, Universidad de Las Palmas de Gran Canaria

ABSTRACT

This article highlights the importance of generic and thematic competences when translating commercial texts. It focuses specifically on the relevant theoretical framework for international marine cargo insurance and the genres produced within any claim procedure. The aim is to inform translators about the situational context and the documents involved when loss or damage to goods is incurred, and thus enable a greater command of the subject matter and tenor of discourse. Also highlighted is the importance of understanding the standardisation of words or expressions used in International Trade and Maritime Law with English as the lingua franca, together with the need to apply the correct translation strategies for the final purpose of the translation.

KEYWORDS

Marine cargo insurance, commercial translation, thematic competence, generic competence, claims procedure, standardisation.

1. Introduction

Commercial translation is a subfield of Translation Studies which according to Mayoral (2007: 33, in Gallego et al. 2016: 38) takes place in the context of commercial transactions and therefore it is related to a restricted group of documents which entail very similar forms and functions (payment documents, guarantees, transport documents, invoices, etc.). As suggested by most key translation competence models (EMT Expert Group 2009: 4; PACTE 2005: 610; Göpferich 2008: 155), both thematic and generic sucompetences need to be accounted for in the commercial translation training.

Therefore, the focus of this paper is to address the main problems encountered by novice translators or translation students when attempting to understand a marine cargo insurance-related commercial document, the subject area in which it is framed and the range of genres used in this field of discourse in order to guide them towards appropriate translation solutions.

Consequently, the general purpose of this article is to help build generic and thematic competence in commercial translation that will enable future translators or translation students (at the Masters Degree level) to handle commercial genres, bearing in mind the scant attention they are afforded. We will focus on the area of the international shipping industry, since around 90% of world trade is carried out by this means. The present discussion also intends to highlight the standardisation of expressions, aimed at facilitating international communication, as a linguistic feature typical of the documents produced in international trade and maritime law with English as the lingua franca. This paper first underlines the importance of generic competence as part of students’ commercial translation competence. Readers are later introduced to contextual information about marine cargo insurance such as international logistics and the parties involved in waterborne transport and next Incoterms. The article ends with the presentation of the main genres produced in marine cargo insurance claims before offering recommendations on translation strategies or types of solution translators should deploy depending on the translation purpose.

2. Generic competence in commercial translation

Generic competence is one of basic abilities translators should develop as part of their translation competence (Hurtado Albir 1999; Kelly 2002; García Izquierdo (ed.) 2005; Montalt Resurreció et al. 2008; Ciapuscio 2012; Suau Jiménez and Gallego Hernández (eds) 2017). In this sense, generic competence can be best defined as “the ability to exploit successfully a range of genres to achieve the goals of a specific professional community” (Goźdź-Roszkowski 2016: 53). Foreign trade experts (e.g. customs brokers or agents) internalise generic competence because they are aware of the variety of text genres used in their professional practice and know how to use them to conduct their work in a smooth and timely manner. As a result, “translators should be able to recognize the generic integrity of the texts they deal with” (Goźdź-Roszkowski 2016: 54).

In fact, a genre-based analysis has been applied to specialised translation by many authors since the late 1980s, such as Bédard (1987), Titov (1991), Hatim and Mason (1995), Trosborg (1997), Hatim (1997), Borja Albi (2013) for it allows for the observation of linguistic patterns used for a specific genre by a particular discourse community. In this context, it is worth mentioning the Gentt (Géneros Textuales para la Traducción) research team of Universitat Jaume I, whose main focus is the multilingual study of genres in professional legal, medical and technical contexts1. Moreover, we agree with Goźdź-Roszkowski when he suggests that:

(…) analyzing a genre set which was employed at different stages in an actual professional practice could be one of the sources for acquiring generic competence. A range of texts linked by the same institutional goals and the network of legal professionals (…) helps to highlight intertextual relationships that a given text may have with the other texts (2016: 65)

Borja Albi (2013), who has extensively researched legal genres, likewise underlines the importance of text corpora for legal translation. Biel (2018) points out the applications of genre analysis in translator training and the internalisation of genre knowledge as an important component of professional translators’ ability to perform effectively. Similarly, many researchers agree with the idea that a text taxonomy can be understood as a useful tool for developing skills that will enable professional translators to cope with the translation of text types for specific purposes. In the author’s opinion, a commercial text taxonomy can also help to design a commercial translation training programme and provide the necessary background knowledge to enable future translators to work within this specific field of discourse. To conclude, it is worth studying the genres produced in this specific field of discourse since they have been barely studied for translation purposes until now.

Socorro Trujillo provides a taxonomy of commercial texts used in international trade divided into five macrogenres: informative, official, transport and financial documents and other forms of international contracts (2008: 45-124). With regard to the documents accompanying transport documents, the author includes the following insurance genres: a survey report, an insurance policy and an insurance certificate (Socorro Trujillo 2008: 103-105). However, there are other subgenres linked to a marine cargo insurance claim. All of them will be presented and explained here.

A survey conducted in Spain by Del Pozo Triviño (2009: 166-176) with shipping agencies, stevedores, ship owners, lawyers, translation agencies and freelance translators shows that around 70% of respondents usually translate texts that relate to International Maritime Law in the English-Spanish language combination. English is certainly the lingua franca of the International Maritime Organization (IMO)2. When asked about the most frequently translated texts, out of the 11 listed, the Sea Protest was in first place, the Bill of Lading (B/L) — explained in section 4.1 was third, the Single Administrative Document (SAD) fifth, the marine insurance documents eighth, followed by the Charter Party (C/P). As we will see, some of these documents are linked to marine cargo insurance claims.

3. Contextual information about marine cargo insurance

3.1. International logistics

In order to understand the subject matter, one needs to know that:

The heart of maritime law, in its international context, lies in the transportation of goods and passengers for compensation. Ships today are larger, faster, and, with the advent of “containerization,” can carry cargo more safely than vessels of 100 years ago. (Force 2013: 43)

Logistics entails the physical movement of products from their point of origin to the place of receipt by end users (Dorta González 2006: 5). Therefore, transportation is the key element in the international logistics chain. When exporting or importing goods, it is very important to hire a suitable handling organisation to ensure that the packaging and labelling complies with standards in order to avoid problems. Both exporters and importers must also be aware of their respective responsibilities and what specific export and import documentation will be required.

The term “container” has two different meanings, according to the online Business Dictionary: “(i) a bottle, can, etc. which can hold goods and (ii) a very large metal case of a standard size for loading and transporting goods on trucks, trains, and ships.” Standard intermodal containers are fundamental in international trade (Velasco Gatón 2017: 518). According to Dedola Global Logistics, TEU stands for Twenty-Foot Equivalent Unit, which can also be used to measure a ship’s cargo carrying capacity. Internationally, the dimensions of one TEU are equal to that of a standard 20′ shipping container; 20 feet long, 8 feet tall. Dedola Global Logistics considers that, usually 9-11 pallets, portable platforms on which goods can be stacked, fit into one TEU. Additionally, there is a standard container of the same width but double the length (forty feet), called a 40-foot container, which equals one forty-foot equivalent unit (often FEU or feu) in cargo transportation (Business Dictionary). Two TEUs are considered equal to one FEU, forty-foot-equivalent unit (ISO 6346: 1995). Translators should bear in mind that both TEUs and FEUs are abbreviations for measuring containers in international transport, as explained in the online Logistics Glossary, and “the output of container ports” (Wayne 2009), and that there are different kinds of containers (high cube, reefer, tank or standard or dry van containers, etc.) regulated by ISO 6346:1995. In both cases, the translation strategy to be applied will depend on the specific translation purpose as we detail in section 4.2.

There are also four ways of importing and exporting goods — road, rail, air and sea — and it is possible to use more than one type of transport, named multimodal or combined transport. In such cases, the transportation of goods is covered by a single contract (B/L) but performed using at least two different means of transport where the carrier is liable for the entire carriage. Different rules and conventions exist for each method of transport. Translators therefore need to be aware of such differences and the implications these have. International transport of goods by road is governed by the Convention for the Contract of the International Carriage of Goods by Road (CMR Convention) signed in Geneva in 1956. There is no European Union regulation with respect to indemnification for road freight. Meanwhile, the international transport of goods by rail is regulated by the Uniform Rules concerning the Contract of International carriage of Goods by Rail (CIM Convention), signed in Bern in 1980. The European Commission’s Trade Helpdesk guide (2018) points out that the 1968 International Convention on Bill of Lading, better known as the Hague Rules or the Brussels Convention, dictates the marine carrier's responsibilities when transporting international goods.

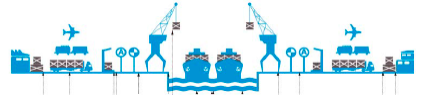

The means of transport, supporting documents, insurance and packaging, among others, demand great professionalism from those responsible for logistics and forwarding. The issue becomes more complex as a result of barriers on imports, in accordance with the prevailing law in some countries. Figure 1 exemplifies the sequence of activities in the international transport of goods (the international logistics management).

Figure 1. Representation of the international logistics process (Dorta González 2014: 6)

These are: loading and domestic transport in the country of origin, customs clearance, stowage in the international means of transport, international transport, unloading at the place of delivery, import customs clearance and inland taxes (tariffs, etc.), inland transport and unloading in the place of arrival (Dorta González 2014: 6).g>

3.2. Marine Cargo Insurance

Baughen defines marine cargo insurance as:

a contract whereby the insurer undertakes to indemnify the assured in manner and to the extend thereby agreed, against marine losses, that is to say, the losses incident to marine adventure. It may also be extended so as to protect the assured against losses on inland waters or on any land risk may be incidental to any sea voyage. (2009: 256)

Normally, goods arrive at their destination without incident. However, in the event that something undesirable happens while the merchandise is being stored or while in transit — anything from natural disasters to vehicle accidents, loss, damage or theft, or even acts of war — the consequences can be devastating for the exporter/importer or business if they do not have the appropriate cargo insurance coverage. As clarified by the international insurance company Zurich, marine cargo insurance, also known as freight, marine or shipping insurance, ”covers the risks of loss or damage to goods and merchandise while in transit by any method of transport — sea, rail, road or air — and while in storage anywhere in the world between the points of origin and final destination.” Lloyd’s agency, the incorporated society of insurance underwriters in London which provides services to the global marine market, states with regard to compulsory insurance coverage for all Lloyd’s agents that:

All policies of insurance on cargo will set out the risks (perils) that the underwriters provide cover against. (…) [I]t will usually be the case that the insurance will be subject to Institute Cargo Clauses (ICC). These are standard wordings agreed by the London market and are widely used, or closely copied, around the world. (2009: 8)

Such globally standardised Institute Cargo Clauses (ICC) are customary in insurance documents — even in those written in languages other than English — and adopted as standard terms by many international marine insurance organisations, including the Institute of London Underwriters (ILU) and the American Institute of Marine Underwrites (AIMU), among others. This is not only because English is the lingua franca but also due to the influence of London in global insurance and reinsurance with regard to non-life insurance covers. For example, the London based Protection and Indemnity Insurance clubs, P&I clubs, which are mutual insurance associations for ship owners and charterers, specialise in marine insurance covering as much as “90% of the world maritime tonnage” (Tan 2006: 41). ICC A provide all risks cover, subject to specific exclusions, whereas the insurance cover provided under ICC B is greater than that of ICC C, which is the most restrictive one (Brown and Novitt 1985: 305)3.

3.3. Parties or ‘players’ in waterborne transport

Since the object of this study is marine cargo insurance, this section will discuss the parties involved in marine transport. As explained by Force (2013: 43), the ‘players’ in waterborne transport include: the ‘shipowner’ who is the person who owns a merchant vessel; the ‘charterer’ who contracts to use the carrying capacity of a vessel; ‘shipper’ is the party who wants their goods to be transported from one place to another; ‘consignee’ is the receiver of the goods; and ‘freight forwarders’ arrange the transportation on behalf of a buyer or seller.

In addition to the aforementioned parties, a few more can be added, such as the ‘master,’ ‘carrier’ and the ‘ship agent,’ where ‘master’ is the person who has the command of a vessel, i.e. the captain, and the ‘carrier,’ as defined in Article 1 of Hamburg Rules 1978, “means any person by whom or in whose name a contract of carriage of goods by sea has been concluded with a shipper.”

The 2018 Amendment to Article VII(2)(b) of the IMO FAL Convention of 1965 on Facilitation of International Maritime Traffic defines the ship agent as “the party representing the ship’s owner and/or charterer (the Principal) in port, including preparation and submission of documentation and customs formalities.” Force (2013: 43) also refers to “nonvessel operating common carriers” (NVOCCs).

Finally, Article 14 of Hamburg Rules imposes an obligation on the carrier to issue a bill of lading B/L to the shipper when the carrier or actual carrier takes the goods into his or her or her charge (Baughen 2009: 137). Banks are also important links in the transport document chain when payment for the goods is being made by means of a Letter of Credit, since the B/L may be used as a negotiable instrument for payments between a buyer and seller using such a method of payment (López Calvo et al. 2017: 398).

3.4. Incoterms

As indicated above, packaging, labelling, transportation, etc. are important aspects of international logistics process, as is insurance coverage for the whole shipping chain. Another important aspect related to logistics is agreeing upon the exact point of delivery in the destination country. Incoterms 2010 are key elements in this respect. They are also crucial in international cargo insurance. Depending on the Incoterm agreed in a commercial transaction, the responsibilities will lie either with the exporter, the shipper, the importer or consignees of goods. Therefore, it is essential for shippers to know the exact status of their shipments in terms of ownership and responsibility. According to the International Chamber of Commerce (ICC)4:

The Incoterms rules have become an essential part of the daily language of trade. They have been incorporated in contracts for the sale of goods worldwide and provide rules and guidance to importers, exporters, lawyers, transporters, insurers and students of international trade.

The Incoterm rules are intended primarily to avoid costly misunderstandings by defining obligations, costs, and risks involved in the international delivery of goods from the seller to the buyer. There are eleven widely used and internationally approved Incoterms by the International Chamber of Commerce (ICC). Only four Incoterms apply to sea or inland waterway transport — these areFAS, FOB, CFR and CIF. As previously mentioned, Incoterms delineate where the responsibilities of shippers, sellers, buyers and consignees begin and end. Therefore, as explained by the International Trade & Transportation Glossary, “it is vital for sellers and buyers to arrange insurance on their goods while the goods are in their ‘legal’ possession. Lack of insurance can result in wasted time, lawsuits, and broken relationships.”

4. The cargo claims procedure

According to Arroyo Martínez (2014: 367-374), when damage occurs to goods, the actions to be taken by the insured are as follows:

- to state an occurrence of a loss or damage;

- to request a survey (contact an insurer correspondent);

- to mitigate damage.

In dealing with cargo claims, it is important to remember that international rules apply to the carriage of goods by sea, such as the Hague-Visby, Rotterdam or Hamburg Rules. The legislation to be applied depends on what Rules the particular country has ratified. The Hague-Visby Rules (1968), for example, specify the obligations of the carriers (maintenance of seaworthiness and cargo care throughout their loading, navigating, discharging and delivering operations). Claims are also reviewed under limited liability as per Bill of Lading terms and conditions and International Conventions. This means that when the cargo is not insured by the exporter/importer, claims will solely be dealt with on the basis of the shipping company’s liability as the carrier.

In the eventuality that goods are destroyed, damaged, or stolen, a marine insurance claim in writing should be made to the insurance company immediately so that they can take the necessary steps to determine the loss. Claims may be submitted either by the legal owner of the damaged freight, or an entity accepting risk of loss in transit, or a legal proxy (called subrogation). Therefore, a subrogation is the right of the insurer to any recourse which the assured may have against third parties wholly or partly responsible for the loss in respect of which a claim has been paid (Force 2013: 199).

The claim must be made to the carrier or to the shipping company. A formal acknowledgement also needs to be received from both the insurer and the shipping company. It may be necessary to make a claim to all the carriers in the transit chain. In addition, there may be occasions where third parties other than the carriers (stevedores, port authorities, customs authorities, etc.) may be liable for loss or damage. All documentation pertaining to claims against such third parties must be preserved. Failure to comply with this requirement will prejudice insurance claims. Finally, for underwriters to be able to conclude the claim with the carrier or a third party — after having paid for the claim to the insuree under subrogation — the former must be held responsible, in writing, by the claimant, for the loss within a specific time frame (Arroyo Martínez 2014: 375). Below, as an example, we present the steps to be followed in claims procedure according to Maersk shipping company, the world’s largest container shipping line: 1) Immediately notify the insurer or underwriter, or contact the shipping line customer service; 2) Appoint a surveyor and arrange for joint/bilateral inspections of the damaged cargo; 3) Minimise and prevent further losses; 4) Collect documents regarding the claim 5) Submit a substantiated and quantified claim; and 6) Protect against time bar.

As can be seen, there are a number of documents that will be necessary for filing a marine insurance claim. These will be dealt with in next section.

4.1. Main genres within a claim procedure

in this section, we deal with the most common genres present in a claim procedure taking into account their dominant contextual focus (Hatim and Mason 1990: 145-146). Firstly, a prompt notice of claim by the insuree is required (Mishra and Mishra 2016: 327). The purpose is to clearly define details of the loss, including the commodity damaged, the extent of damage, and the value of the damage. It should include the itemisation of the claim and explanation of claim circumstances. Subsequently, the following documents or genres are to be submitted by the insuree in order to ensure an expeditious settlement of a claim by the insurance company:

- Original Insurance Policy or Certificate.

- Bill of Lading (or other Carrier’s Receipt).

- Survey report.

- Original Invoice and Packing List together with shipping specification or Weight Notes.

- Bill of Sale.

- Sea Protest.

- Letter of Subrogation(Mishra and Mishra 2016: 327-328; Mishra et al. 2013: 42).

Mishra et al. (2013: 40) also point out that all correspondence exchanged with carriers and other parties regarding the liability for the loss or damage should also be forwarded. Below we provide a definition of these marine insurance interrelated documents to help understand their intertextual connections as well as their situational context.

Insurance Certificate. According to Mishra and Mishra, it is a document issued by an insurance company covering a specific shipment. It states the “terms and conditions of the cargo insurance and is subject to the terms and conditions of the underlying cargo policy. It is used when evidence of insurance is required, especially by a bank issuing a Letter of Credit” (2016: 362).

Marine Insurance Policy. It is a document which provides evidence of the contract of marine insurance between the insurer and the assured whereby the insurer undertakes to settle claims properly recoverable in accordance with the risks covered and the conditions set out in the policy document (Brown 2004: P13). According to the UNCTAD, although the particulars which every cargo policy should contain are a matter for the national legislation of the country where the policy is issued, a marine insurance policy should normally contain the following items:

- a name of the insured or a name of the person or body who contracts the insurance on his own or other’s behalf;

- name of the insurer or insurers;

- subject matter of the insurance, namely goods shipped or to be shipped, their nature, packing, quality, etc.;

- the sum insured;

- voyage or period of time or both, as the case may be;

- name of the vessel or description or another conveyance by which the goods are transported, including the proposed sailing date or the attachment of the risk;

- perils covered and excluded;

- loss payee if property is mortgaged;

- in addition, policies may or may not show the premium rates agreed (1975: 20-21).

Bill of Lading (B/L). It is the evidence of the contract of carriage entered into between the Carrier and the Shipper or Cargo Owner in order to carry out the transportation of the cargo as per the sales contract between the buyer and the seller (Gabaldón García and Ruiz Soroa 1999: 450-452). A B/L is also a receipt of goods because it is issued by the carrier or their agent to the shipper or their agent in exchange for the receipt of the cargo. It is also a document of title, which means that the goods may be transferred to the holder of the B/L, which then gives the holder of the B/L the right to claim the goods or transfer them to someone else (Alas 1983: 40).

Survey Report. It is a detailed document, compiled by a surveyor, of the cause of the loss, valuation, etc. quantifying the amount of the loss. It is a report of an expert, issued by an independent party such as an assessment and cause of the damaged cargo on which a claim has been lodged (Branch 2004: 786).

Commercial Invoice. The invoice accompanying the consignment is issued by the seller of the goods. This will be used to establish the purchase price of goods and to confirm the terms of sale to ensure that an insurable interest applies (Hernández Muñoz 2002: 246).

Packing List. This document provides a breakdown of the consignment showing the number of units shipped in each package along with their weights (Hernández Muñoz 2002: 319).

Bill of Sale. It is a registered transfer of goods to a person for some consideration empowering him/her to dispose of them upon non-fulfilment of certain conditions (Branch 2004: 73).

Sea Protest. It is a document containing an account of events or statement of facts, describing the current situation or consequences of some wrongful act(s), which happened usually contrary to the efforts of the master’s crew (Pujol Bengechea (ed.) 2000: 271). Therefore, some companies adopt a statement of facts. Protests can also be made by the merchant against the master.

Letter of Subrogation. It is a document giving authority to the insurer to sue a third party in the name of the assured for damages when a third pary is responsible for a loss which has resulted in a claim under the policy (Brown 1989: L13).

Subgenres other than those listed above can also be encountered, depending on the circumstances of the claim. They are listed by W K Webster & Co Ltd, a marine and insurance transit claims specialist, whose origins date back to pre-1861, and include the following: vessel's outturn report (written statement by a stevedoring company in which the condition of cargo discharged from a vessel is noted along with any discrepancies in the quantity compared with the vessel’s manifest, Branch 2004: 603); a container damage report; a tally sheet (record of the number of cargo items together with the condition thereof at the time it is loaded into or discharged from a vessel, Branch 2004: 793); written confirmation of non-delivery from a carrier; police statement (in the event of theft), etc.

Nevertheless, as W K Webster & Co Ltd, notes, the customer normally “will be guided by the [insurance] company as to what additional documents may be required once the claim has been reported to them.” Thus, not all of these additional documents are applicable in every case. In fact, other extra documents may be required depending on the nature of the goods or other factors. Maersk Line, for example, includes some additional documents such as the following: Salvage Receipt or Destruction Certificate (to confirm mitigation efforts or destruction); Temperature Records (if applicable, to assess any deviation in cargo temperature); Unloading Tally (to substantiate cargo quantity at unloading); Delivery Receipt (to verify receipt, check seal integrity and examine any exceptions); equipment interchange receipts and/or; Export/Import Declaration (the Single Administrative Document, SAD in the EU or a copy of the Customs Entry documentin the USA).

At this point, we can affirm that a number of genres are produced within a claim procedure, and that these form a set of documents or a cluster (cf. Bazerman 1994) with apparent intertextual relationships even though they separately have very different internal structures and functional purposes. Together, they represent a highly structured and conventionalised communicative event.

4.2. The translation of standardised expressions in marine cargo insurance-related documents

In this section, we deal with the main translation strategies, procedures or solutions types that can be deployed when translating globally-standardised specialised words or expressions present in the marine insurance documents produced in the field of International Maritime Law. Some examples have already been mentioned in this article, such as: TEU or FEU, the Institute Cargo Clauses together with the Incoterms. According to Lörscher (1991, qtd. in Fernández Guerra 2012: 124), among other authors, translation strategies are usually defined as procedures leading to the optimal solution of a translation problem. Yet, the strategy to be deployed depends on the aim of the translation and the potential target reader (Reiss and Vermeer 1984). As recommended by Nord (2006: 59), the commercial translator will have to analyse the target expertise conditions (of the target readers) for whom the translation is needed. The translation of marine insurance documents may be used, e.g., in a communicative situation where not all the target readers are equally aware of the subject matter.

Some of the most representative taxonomies of translation procedures, strategies or types of solutions (Vinay and Darbelnet 1984; Vázquez Ayora 1977: 257-385 or; Newmark 1988: 81-93) include procedures applied to the translation of these standardised specific terms, such as literal translation (‘franco a bordo’, for ‘free on board’ on an invoice) or transference (‘TEU’ in a B/L), when a term is ‘copied’ into the target text. The problem with regard to literal translation is that the communicative purpose may not be achieved because these English standardised terms (FOB rather than ‘franco a bordo’) are internationally recognized within the expert discourse community. Thus, translators should bear in mind that these English equivalents are commonly used globally and so avoid unnecessary clarification.

In an unlikely, however not impossible, situation where the translation skopos requires it (for example, in the case of an unknown word by the target reader), notes or additional information may be supplied in order to clarify a complex extralinguistic context known to the reader of the original text, however requiring clarification for the reader of the TT (Vázquez Ayora 1977: 352; Newmark 1998: 91; Pym 2018: 44). In fact, as suggested by Newmark, a third good solution might be a combination of two options, i.e. providing a linguistic borrowing or loan word plus additional information (within the text; notes at the bottom of the page; notes at the end of the chapter or notes or glossary at the end of the book). A possible explanation for the borrowed term, ‘FOB’ might be that it stands for Free on Board and is an Incoterm rule with universal meaning for buyers and sellers around the world, created by the International Chamber of Commerce (ICC 2010).

To sum up, translators, we feel, should not be limited in their choice of what translation strategies to apply for a specified translation task. In fact, for the Skopos theory, such changes are a legitimate part of “translatorial action” (Reiss and Vermeer 1984; Holz-Mänttäri 1984 qtd. in Pym 2018: 48).

5. Conclusions

This article has underlined the role of generic competence and thematic expertise in commercial translation. It has emphasised that term research for translation purposes should account for the extralinguistic context of International Trade and Maritime Law in which they are framed.

As we have seen, although there are common documents to be presented when a claim is reported (Insurance Certificate or Policy, Packing List, Bill of Lading, Survey Report, etc.), other additional documents may be required depending on the nature of goods or other factors (Salvage Certificate, Destruction Certificate, Lab Certificate, SAD, etc.). Thus, an interdisciplinary translation task is carried out in commercial translation as a whole and more particularly when a marine cargo insurance claim is settled where genres with predictably different communicative purposes and with different internal structures enter into relationships and interact (transport documents, correspondence or insurance contracts). Therefore, the documents produced when an international loss or damage to goods is incurred can be understood as a “system of genres” or “interrelated genres that interact with each other” (Bazerman 1994: 97) and are linked to each other by a communicative purpose: to ensure expeditious settlement of the claim. In addition, understanding the situational context where these text types are produced help shape the background knowledge needed to cope with the translation of this system of interdependent genres (Bazerman 1994) or genre chain (Fairclough 2003: 216).

Moreover, as the London market is the world's insurance and reinsurance leader for large risks and non-life insurance covers, English is used worldwide, for example as in the case of the Institute Cargo Clauses (ICC). English also seems to be the universal language of communication for the International Maritime Organization (IMO) and the primary working language of trade as exemplified in how container capacity is measured internationally (TEU or FEU). In addition, the Incoterms issued by the International Chamber of Commerce (ICC) and some international conventions and uniform rules are also formulated in English and used worldwide. As a result, one of key linguistic features of International Maritime Law and of related marine insurance documents is high standardisation which is mediated through English. Translators who work with such challenging texts should be aware of standardisation in both English and their native languages and adjust their strategies to the skopos of the text to facilitate smooth communication between experts and other types of target text recipients.

References

- Alas, César (1983). Diccionario jurídico-comercial del traansporte marítimo. Gijón: Servicio de publicaciones de la Universidad de Oviedo.

- Arroyo Martínez, Ignacio (2014). Compendio de derecho marítimo (Ley 14/2014 de Navegación marítima). Madrid: Tecnos.

- Baughen, Simon (2009). Shipping Law. 4th ed. London/New York: Routledge Cavendish.

- Bazerman, Charles (1994). “Systems of genres and the enactment of social intentions.” Aviva Freedman and Peter Medway (eds) (1994). Genre and the New Rhetoric. London: Taylor and Francis, 79-101.

- Bédard, Claude (1987). Guide dénseignment de la traduction technique. Montreal: Linguatech.

- Biel, Łucja (2018). “Genre analysis and translation.” Kirsten Malmkjaer (ed.) (2018). The Routledge Handbook of Translation Studies and Linguistics. London/New York: Routledge, 151-164.

- Borja Albi, Anabel (2013). “A genre analysis approach to the study of court documents translation.” Linguistica Antverpiensia NS-TTS, special issue on Research models in legal translation, edited byŁucja Biel and Jan Engberg (eds), 12, 33-53.

- Branch, Alan (2004). Dictionary of Shipping: International Business Terms and Abbreviations. London: Witherby.

- Brown, Robert H. and Novitt, John J. (1985). Marine Insurance: Cargo Practice. Vol. 2, 5th Ed. London: Witherby.

- Brown, Robert H (1989). Dictionary of Marine Insurance Terms and Clauses. London: Witherby.

- Ciapuscio, Guiomar (2012). “La lingüística de los géneros y su relevancia para la traducción.” Martha Shiro, Patrick Charadeau and Luisa Granato (eds) (2012). Los géneros discursivos desde múltiples perspectivas: teorías y análisis. Madrid: Iberoamericana, 87-98.

- Del Pozo Triviño, Isabel (2009). “La traducción de documentos marítimos. Clasificación de los principales géneros y marco de análisis.” Sendebar 20, 165-200.

- Dorta González, Pablo (2014). Transporte y logística internacional. Colección TiDES- Técnicas Estadísticas Bayesianas y de Decisión en Economía y Empresa (TEBADM). Gran Canaria/Spain: Universidad de Las Palmas de Gran Canaria (ULPGC). https://accedacris.ulpgc.es/bitstream (consulted 02.01.2019)

- EMT Expert Group (2009). Competences for Professional Translators, Experts in Multilingual and Multimedia Communication. http://ec.europa.eu/dgs/translation/ (consulted 25.04.2019)

- Fairclough, Norman (2003). Analysing Discourse. Textual analysis for social research. London: Routledge.

- Fernández Guerra, Ana B. (2012). “Crossing Boundaries: The Translation of Cultural Referents in English and Spanish | Request”. A Journal of Literary Studies and Linguistics 2(2), 121-138.

- Force, Robert (2013). Admiralty and Maritime Law. New Orleans: Judicial Federal Judicial Centre.

- Gabaldón García, Jose Luis and Ruiz Soroa, Jose María (1999). Manual de derecho de la navegación marítima. Madrid: Marcial Pons.

- Gallego Hernández, Daniel, Geoffrey S. Koby and Verónica Román Minguez (2016). “Economic, financial and commercial translation: An approach to theoretical aspects. A survey study.” MonTI 8, 35-59.

- García Izquierdo, Isabel (ed.) (2005). El género textual y la traducción. Reflexiones teóricas y aplicaciones pedagógicas. Berne: Peter Lang.

- Goźdź-Roszkowski, Stanisław (2016). “The Role of Generic Competence and Professional Expertise in Legal Translation. The Case of English and Polish Probate Documents.” Studies in Logic, Grammar and Rhetoric 45(1), 51-67.

- Göpferich, Susanne (2008): Translationsprozessforschung: Stand, Methoden, Perspektiven (Translationwissenschaft 4). Tübingen: Narr.

- Hatim, Basil (1997). Communication Across Cultures: Translation Theory and Contrastive Linguistics. Exeter: University of Exeter Press.

- Hatim, Basil and Mason, Ian (1990). Discourse and the Translator. London: Longman.

- Hatim, Basil and Mason, Ian (1995). Teoría de la traducción. Una aproximación al discurso. Barcelona: Ariel.

- Hernández Muñoz, Lázaro (2002). Diccionario de comercio internacional. Madrid: Instituto Español de Comercio Exterior (ICEX).

- Hurtado Albir, Amparo (1999). Enseñar a traducir. Metodología en la formación de traductores e intérpretes. Barcelona: UAB.

- Kelly, Dorothy (2002). “Un modelo de competencia traductora: bases para el diseño curricular.” Puentes 1, 9-20.

- Lloyd’s Agency. (2009). Cargo claims and recoveries. Module 3, 1-174. https://docplayer.net/7741657-Cargo-claims-and-recoveries-module-3.html (consulted 20.04.2018).

- López Calvo, Mª José, Morán Serrano, Miguel and Maite Seco Benedicto (2017). Financiación de la internacionalización. En Arteaga, Jesús (ed.) Manual de internacionalización. Madrid: ICEX, 373-468

- Mishra, M. N. and Mishra Sadasiv (2016). Insurance Principles and Practise. 22nd ed. New Delhi: S. Chand an Co Ltd.

- Mishra, Sadasiv, Aloke Jha, Singh Sanjiv and Vikas Patil (2013). Guide to marine cargo insurance. Mumbai/India:The new India insurance Co. Ltd.

- Montalt Resurreció, Vicent, Ezpeleta Piorno, Pilar and Isabel García Izquierdo (2008). “The Acquisition of Translation Competence through Textual Genre.” Translation Journal, 12 (4). https://translationjournal.net/journal/46competence.htm (consulted 20.03.18)

- Newmark, Peter (1988). Approaches to Translation. Hertfordshire: Prentice Hall.

- Nord, Christiane (2006). “Translating for Communicative Purposes across Cultural Boundaries.” Journal of Translation Studies 9(1), 59-76.

- PACTE (2005): “Investigating Translation Competence: Conceptual and Methodological Issues.” Meta: Translators’ Journal 50(2), 609-619.

- Pujol Bengechea, Bruno (ed.) (2000). Diccionario de comercio exterior. Bolsa- Banca. Madrid: Editorial Cultural S.A.

- Pym, Anthony (2018). “A typology of translation solutions.” The Journal of Specialised Translation 30,41-65.

- Reiss, Katharina and Vermeer, Hans J. (1984). Fundamentos para una teoría functional de la traducción. Madrid. Akal.

- Socorro Trujillo, Karina (2008). Aspectos textuales y terminológicos de documentos mercantiles del comercio internacional: herramientas aplicables a la formación de traductores. Gran Canaria/Spain: Servicio de publicaciones de la Universidad de Las Palmas de Gran Canaria.

- Suau Jiménez, Francisca and Gallego Hernández, Daniel (eds.) (2017). Géneros textuales y competencias: nuevas perspectivas en la formación de traductores de textos especializados, a special issue of Sendebar 28.

- Tan, Alan Khee-Jin (2006). Vessel-Source Marine Pollution. The Law and Politics of International Regulation. Cambridge: Cambridge University Press

- Titov, Vladimir (1991). “Estudio del estilo científico en español: bases metodológicas.” Estudios humanísticos. Filología 13, 135-144.

- Trosborg, Anna (1997). “Text typology: Register, Genre and Text Type.” Trosborg, Anna (ed.) (1997). Text Typology and Translation. Amsterdam/Philadelphia: John Benjamins, 3-23.

- UNCTAD (United Nations on Trade and Development) (1975). Insurance. Marine cargo insurance. Study by the UNCTAD secretariat. http://unctad.org/en/PublicationsLibrary/tdbc3d120_en.pdf (consulted 2.05.2018)

- Vázquez Ayora, Gerardo (1977). Introducción a la Traductología. Washington: Georgetown University Press.

- Velasco Gatón, Natalia (2017). Transporte y Logística internacional. Jesús Arteaga Ortiz (ed.) (2017). Manual de Internacionalización. Madrid: ICEX, 468-560.

- Vinay, Jean-Paul and Jean Darbelnet (1984). Comparative Stylistics of French and English. A methodology for translation. Amsterdam/Philadelphia: John Benjamins.

- Wayne, K. Talley (2009). “Container port efficiency and output measures.” Paper presented at the Conference of the International Association of Maritime Economists. Dalian Maritime University, Dalian, China.

Websites and Legal Acts

- Business Dictionary. www.businessdictionary.com (consulted 20.01.2019).

- Convention for the Contract of the International Carriage of Goods by Road (CMR). Geneva 19 May, 1956. http://www.unece.org/fileadmin/DAM/trans/conventn/cmr_e.pdf (consulted 4.02.2019).

- Dedola Global Logistics (2011). “What is a TEU?” https://bit.ly/2O5hcRF (consulted 13.10.2018).

- European Commission (2018). Trade Helpdesk. Documents for customs clearance. https://trade.ec.europa.eu/tradehelp/documents-customs-clearance (consulted 21.04.2018).

- GENTT, http://www.gentt.uji.es/ (consulted 9.06.2019).

- International Chamber of Commerce (ICC) (2010). Incoterms Rules 2010. https://iccwbo.org/resources-for-business/incoterms-rules/incoterms-rules-2010/ (consulted 10.03.2018).

- International Trade & Transportation Glossary. Foreign Trade Online. htts://www.foreigntrade.com/reference/incoterms.cfm/ (consulted 7.05.2018).

- IMO (International Maritime Organisation) (2019). IMO Standard Marine Communication Phrases. http://www.imo.org/en/OurWork/Safety/Navigation/Pages/ (consulted 1.5.2018).

- IMO (International Maritime Organisation) (2019). FAL Convention on Facilitation of International Maritime Traffic (1965). http://www.imo.org/en/About/Conventions/ListOfConventions/Pages/Convention-on-Facilitation-of-International-Maritime-Traffic-(FAL).aspx (consulted 7.05.2019).

- ISO 6346: 1995 (1995). Freight containers - Coding, identification and marking. ISO/TC 104/Sc 4. https://www.iso.org/standard/20453.html (consulted 30.03.2018).

- Hague Rules (1924). International Convention for the Unification of Cetain Rules of Law relating to Bills of Lading (“Hague Rules”), and Protocol of Signature. https://www.jus.uio.no/lm/sea.carriage.hague.visby.rules.1968/portrait.pdf (consulted 4.02.2019).

- Haghe-Visby Rules (1968). The Hague Rules as Amended by the Brussels Protocol 1968. https://www.jus.uio.no/lm/sea.carriage.hague.visby.rules.1968/plain.txt (consulted 4.02.2019).

- Hamburg Rules (1978). United Conventions on the Carriage of Goods by Sea, 1978. http://unctad.org/en/PublicationsLibrary/aconf89d13_en.pdf (consulted 3.05.2018).

- Logistics Glossary online. https://www.logisticsglossary.com/search/bill+of+sale/ (consulted 13.05.19).

- Maersk Line “Guide to cargo claims handlings.” https://www.maerskline.com/-/.../005-claims-guide-04192017.pdf (consulted 5.04.2018).

- OTIF (Intergovernmental Organisation for International Carriage by Rail) (1980). Contract of International Carriage of Goods by Rail (CIM Convention), Bern 9 May, 1980. https://otif.org/fileadmin/user_upload/otif_verlinkte_files/07_veroeff/01_COTIF_80/cotif-1980-e.pdf (consulted 4.02.2019).

- Rotterdam Rules (2008). United Nations Convention of Contracts for the International Carriage of Goods Wholly or Partly by Sea. https://www.uncitral.org/pdf/english/texts/transport/rotterdam_rules/Rotterdam-Rules-E.pdf (consulted 7.06.2019).

- W K Webster & Co Ltd. “Cargo claims: Reporting a claim.” https://bit.ly/2APhN6v (consulted 8.03.2018).

- Zurich. “What is marine insurance?” https://www.zurich.co.nz/brokers/tools-and-insights/marine-insights/what-is-marine-insurance.html (consulted 18.05.2019).

Biography

Karina Socorro is a Senior Lecturer at the Faculty of Translation and Interpreting of the Universidad de Las Palmas de Gran Canaria (ULPGC). Her PhD thesis (2002) focused on the translation of mercantile papers used in international trade. Her main research fields include commercial and tourist translation. She has published on translation pedagogy and specialised translation in peer-reviewed journals (Monti, Sendebar or Translation Journal) and given seminars and presented papers at the national and international level.

Karina Socorro is a Senior Lecturer at the Faculty of Translation and Interpreting of the Universidad de Las Palmas de Gran Canaria (ULPGC). Her PhD thesis (2002) focused on the translation of mercantile papers used in international trade. Her main research fields include commercial and tourist translation. She has published on translation pedagogy and specialised translation in peer-reviewed journals (Monti, Sendebar or Translation Journal) and given seminars and presented papers at the national and international level.

Email: karina.socorro@ulpgc.es

Notes

Note 1:

www.gentt.uji.es.

Return to this point in the text

Note 2:

This is well illustrated by the IMO standard marine communication phrases (SMCP) which were adopted by the 22nd Assembly in November 2001 as resolution A.918 (22) IMO Standard Marine Communication. Phrases are to be used for navigational purposes where language difficulties arise.

Return to this point in the text

Note 3:

Ocean marine shipments are also subject to the Co-Insurance clause under which the insuree shares in losses to the extent that he/she is underinsured at the time of loss or damage.

Return to this point in the text

Note 4:

ICC is a polysemous acronym since it may also refer to Institute Cargo Clauses.

Return to this point in the text